Charles River Middle Office

The Scalable Core Behind Confident Investment Decisions

Charles River helps leading investment managers scale for growth by consolidating middle office capabilities on our open platform.

Charles River Investment Management Solution (Charles River IMS) provides an alternative to outsourcing with a complete set of middle office capabilities, including investment accounting, cash and position management, collateral management, performance measurement and attribution, and post-trade processing and settlement.

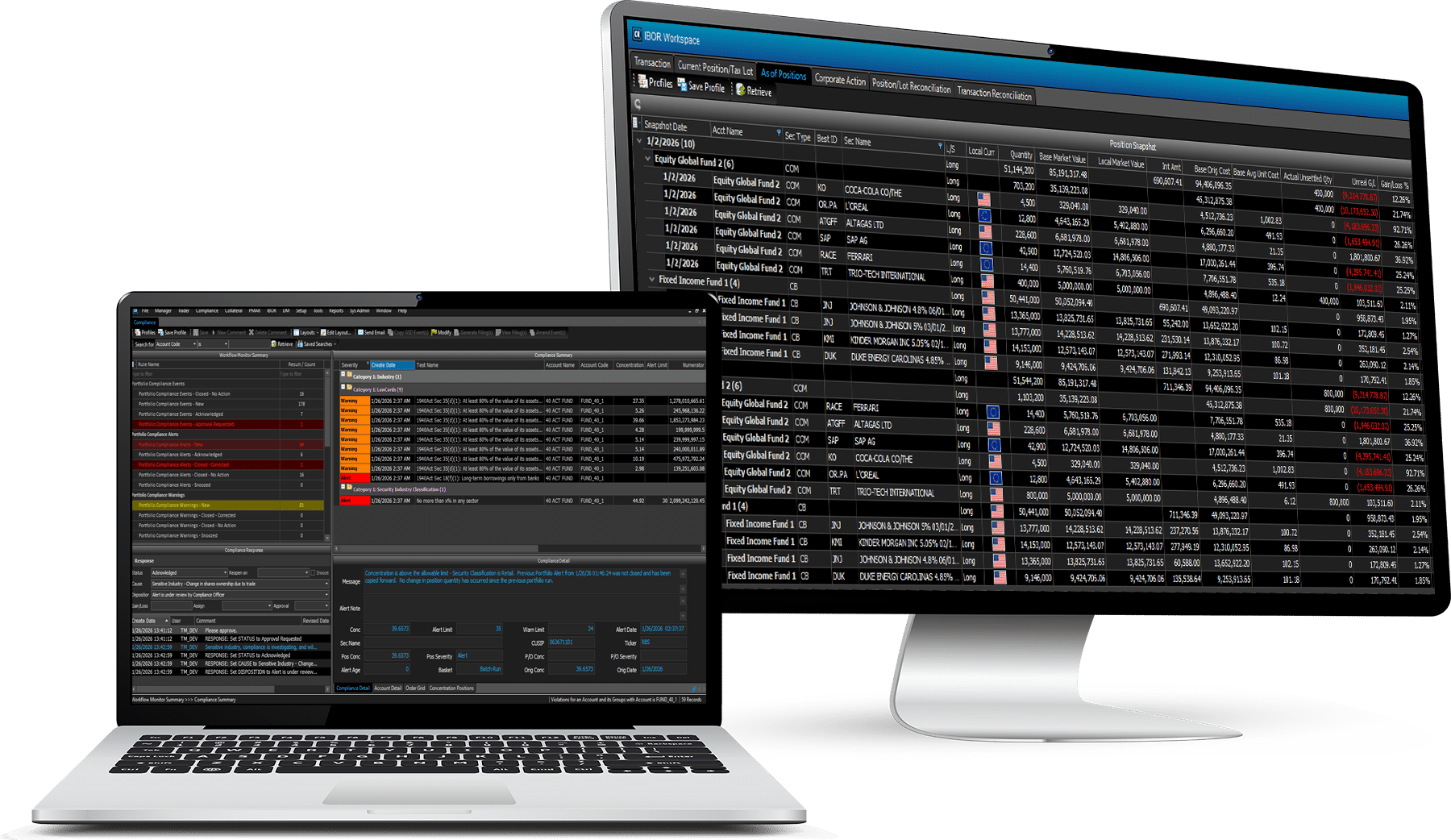

Investment Book of Record (IBOR)

Our Investment Book of Record (IBOR) offering provides the front office with a global, multi-asset view of cash and positions in real time to help drive better decision making and streamline operations.

Designed from the ground up to run securely on the cloud, IBOR’s event-based model allows managers and traders to create multiple aggregation views without multiple books or reconciliations.

The solution manages current and historical positions, with accurate trade date and settlement date positions for a specified point in time, based on transactions and adjustments.

IBOR features Corporate Actions and Reconciliation capabilities. The solution handles automated mandatory and voluntary corporate actions as an overnight process as well as directly from the interface. It helps ensure accurate reconciliation of positions, with flexible, manager-defined matching rules for exception-based workflows.

Accounting

Our offering is designed to simplify middle and back-office operations with true cloud multi-book and multi-asset accounting. Using a consolidated single set of transactional data, it supports multi-book accounting and real-time cash and positions to deliver books of record on any basis, such as GAAP and IFRS, or any other statutory, tax, or currency basis.

Scalable automation workflow and error-detection monitoring ensure data is high-quality and processed quickly, supporting time-sensitive activities such as front office end/start of day, NAV production or shadow NAV reconciliation. It offers data granularity for investments and P&L analysis.

Collateral Management

Charles River enables firms to manage the entire collateral management lifecycle across products on a single platform, from pre-trade analytics and exposure calculations through to margining and settlement.

Fully integrated into Charles River IMS, the solution empowers the front office with decision-making tools embedded in the order management workflow and clear visibility into collateral usage in their portfolios.

Informed by a timely view of available assets, teams can leverage electronic workflows to ensure margin obligations are fulfilled and deadlines are met.

Post-Trade Processing & Settlement

Our post-trade offering helps firms reduce clearing-related risk by automating the post-trade process and providing centralized confirmation, trade matching, and settlement instruction workflows.

Dealers and traders, portfolio managers, compliance, and operations personnel have the same real-time view of all post-trade processing activity and data for each transaction.

Post-trade and settlement capabilities in Charles River IMS include end-to-end confirmation, reconciliation, and settlement workflows. Bidirectional message support and connectivity with SWIFT networks expedite routing of individual trades and allocations to help ensure same-day matching and confirmation.

Enterprise Performance

Enterprise Performance offers clients a fully integrated multi-asset performance calculation engine that enables greater efficiency in performance operations.

The cloud-native solution mitigates data exchange issues, empowering clients with robust and scalable data distribution capabilities. Clients can access multi-dimensional reporting, automated workflows for standard and correction processing, and cross-asset performance, ex-post risk, and attribution-related analytics, with expanded calculation scalability.

Enterprise Performance enables asset managers to handle the complexities in generating performance metrics and analysis across the front, middle, and back office while optimizing performance processes and reporting to both internal and external stakeholders.

50+

Over half of the largest 100 investment managers globally use Charles River technology

$1T+

A top Global Asset Manager improved scale and reduced costs by retiring legacy systems and aligning $1T+ AUM on Charles River.

Explore Our Partner Network

Post Trade Solutions

Cassini Systems

Opturo

Broadridge

TradeNeXus

OSTTRA

Want to learn more? Get in touch.

We're ready to answer your questions. Contact Sales & Marketing by filling out this form.

Follow us on our social channels to stay up-to-date on all Charles River News and Events.

Looking for an Investment Management Solution?

Want to learn more? Get in touch.

We're ready to answer your questions. Contact Sales & Marketing by filling out this form.

Follow us on our social channels to stay up-to-date on all Charles River News and Events.

![]()

Latest Insights

Don’t Start with AI. Start with Friction.

The Hidden Bottleneck in UMA Operations

Private assets for retail investors, what we heard at InvestOps 2026

Private Markets: Establishing a New Paradigm in Wealth Management

Three essentials for data-driven success in modern investment management