Speaking of Alpha: The Evolution of Superannuation Operating Models

Apr 18, 2024

Delivering Member Outcomes at Scale:

Frank Smietana in conversation with Peter Sherriff and Clayton Issitt.

Our Speaking of Alpha series features insights and commentary from State Street Alpha®experts on data, operations, technology and services. Frank Smietana, our head of Thought Leadership, State Street Alpha, leads Peter Sherriff, director of Product Strategy, Asia Pacific, Charles River Development and Clayton Issitt, our head of Client Solutions, Asia Pacific, State Street Alpha, in a discussion about key operational areas impacting superannuation funds, the evolution of fund operating models and how investment and operations teams are addressing these challenges.

Director of Product Strategy, Asia Pacific, Charles River

Clayton Issitt

Head of Client Solutions, Asia Pacific, State Street Alpha

“Regulatory and stakeholder demands are driving superannuation funds to evaluate their operating models, with a focus on improving efficiency, preparing for potential mergers and scaling in a sustainable fashion. Funds are navigating these challenges with different impacts.”

FRANK: Superannuation funds are generally focused on maximising value to their members. When we talk about the evolution of operating models through this lens, what are some of the key business processes and areas of technology that need to be considered?

PETER: Superannuation funds span a broad spectrum of size and sophistication across their investment and operational processes.

At the smaller end of the assets under management (AUM) scale, we see asset owners that rely heavily, or even exclusively, on their external partners and advisors to meet both investment management and reporting requirements. At the opposite end of the spectrum, there are funds that operate much like asset managers in both their global footprint and internalisation of a range of asset management and reporting capabilities.

Every organisation has various combinations of capabilities internalised, as well as an established or evolving operating model aligned with their growth plans. Inevitably, there are organisational barriers to change that need to be overcome. This can be especially challenging for funds that have largely depended on external providers, as they often lack the expertise to navigate associated complexities.

“Superannuation funds span a broad spectrum of size and sophistication across their investment and operational processes.”

FRANK: At the highest level, the asset allocation process and corresponding setting of targets and ranges is a key part of the investment decision-making process and drives member returns. In the context of the spectrum Peter just referred to, what do we see in the industry today and what are the implications for a fund seeking to increase the level of internal delegation?

CLAYTON: For many funds, targets are established at the board level, often based on advice from consultants. The fund then rebalances to these targets on a periodic basis, perhaps within a limited range of tolerance. These targets are generally reviewed and amended on a regular but relatively infrequent basis which may limit the fund’s ability to respond quickly to market conditions or take advantage of investment opportunities in a timely manner.

This can negatively impact the comparative return of funds, and by extension member outcomes, especially during market selloffs and liquidity shocks. Often, as funds increase in size and look for additional capital deployment options, a board-driven process restricts a fund’s ability to expand into new asset classes and geographies.

For the most sophisticated asset owners, responsibility for this process has been delegated to the investment team, which manages Strategy Asset Allocation (SAA) targets as well as shorter term Target Asset Allocation (TAA) goals.

Between these two extremes, we see a range of delegation, with some funds giving discretion over the setting of TAA ranges, while others limit delegation to activities like fund rebalancing, as long as it remains within the SAA range.

PETER: Interestingly, we have seen a small number of firms across Asia Pacific move away from the formal asset allocation approach and towards more of a Total Portfolio Approach (TPA). Moving to TPA represents a significant change in culture as well as process, with the team focusing on the profile of an investment opportunity and its contribution to the overall fund profile, rather than the asset class it belongs to.

Regardless of the level of delegation, we see an impact on the quantity, quality and timeliness of data needed by the investment team and the tools they use to manage investment decisions. At the simplest end of the spectrum, we see widespread dependence on spreadsheets that are fed directly by service provider data. Organisations at the sophisticated end deploy robust data management solutions and investment platforms with integrated risk and performance attribution capabilities.

The key to improved decision-making is the ‘whole of fund’ view, providing organisations with timely and accurate data on exposures and positions across internal and external managers, and public and private assets. Adopting a unified data management platform enables faster, better informed risk and allocation decisions, by reducing the traditional multi-day information lag affecting firms that are reliant on external providers and custodians for fund information.

FRANK: We have just touched on the delegation of the asset allocation process and the variations we see across the industry today. Do we typically see those top-level asset allocation decisions and the internal management of a subset of assets internalised in parallel and what does this mean from a data and technology perspective?

PETER: To some extent, the evolution of a fund’s investment capability goes hand-in-hand with the way the investment decision-making process evolves. We do see exceptions to this with some funds managing a range of investments in-house, while top level decision-making remains with the board.

The most sophisticated asset owners operate as global asset managers in their own right, with investment teams distributed across regions, managing both public and private market assets alongside multi-asset funds. These internal investment teams may be treated as simply another mandate manager by the asset allocation team or, as part of the TPA approach, they may present investment ideas and compete for capital allocation based on perceived contribution to the fund’s risk and return profile.

At the opposite end of the spectrum, where all assets are managed by external asset managers, we tend to see small investment teams that are often given a fairly broad remit to monitor external investments, provide internal board reporting and manage third-party relationships.

A broad range of investments can be managed internally. Whether it involves currency overlays, completion portfolios or individual asset class portfolios such as domestic equity, or directly managing infrastructure or real estate assets, all these have a material impact on the fund’s data and technology requirements.

“The key to improved decision-making is the “whole of fund” view, providing organisations with timely and accurate data on exposures and positions across internal and external managers and public and private assets.”

CLAYTON: We tend to see that when investment capabilities evolve, the definition of what constitutes timely, firm-wide exposure information also changes. For example, firms with limited delegation of their asset allocations and minimal internal asset management may find delayed accounting data adequate. However, firms with more delegated control over their asset allocation and significant internal asset management require an intraday view of exposures, delivered by an investment book of record (IBOR).

A longer term, SAA-only approach can be outsourced to a service provider for managing the rebalancing process, while a more active TAA/Dynamic Asset Allocation (DAA) process requires an enterprise technology solution to support internal investment and operations teams.

This incorporates a shared repository of data that addresses both manager-of-manager and internally managed assets on a common platform, as well as fit-for-purpose views for different teams based on their specific roles. Self-service analysis and reporting tools enable investment professionals to make decisions with greater confidence and collaborate more effectively.

FRANK: The timeliness, accuracy and granularity of data has been a key theme of this conversation. What are some of the considerations funds should have in mind as they evolve their technology platforms and operating models to support this increase in internalised capability?

PETER: The level of responsibility given to an investment team for making asset allocation and investment decisions is closely tied to the in-house data and technology requirements necessary to support those decisions. Where the investment team has very little control and the fund relies heavily on the board and third parties to manage investment and allocation decisions, the information provided by custodians and other service providers is generally timely enough and sufficient in terms of quantity and quality to support internal reporting needs. Typically, any management or manipulation of this data tends to be done in spreadsheets.

As funds internalise more of the investment decision-making process within their own team, there is a corresponding increase in the need for technology and data beyond that provided by the custodian. With internalisation of various aspects of the investment process being the typical evolutionary step, often in a piecemeal fashion to tightly manage costs, each internalised function or asset class is usually deployed on its own specialist or best-of-breed system. This risks creating a siloed and fragmented view of the fund’s overall investments.

We have seen a number of funds pre-emptively increase their technology footprint through data management and warehousing tools to help meet the anticipated increase in reporting and oversight obligations. This enables consolidation of custody data and enrichment with other service providers and internal data.

However, these data repositories often can’t distribute information to the deployed asset class-specific systems due to the siloed nature of these providers. As a result, funds are still heavily dependent on their custodians for an overarching view of the fund and individual investment options.

“As funds internalise more of the investment decision-making process or management within their own team, there is a corresponding increase in the need for technology and data beyond that provided by the custodian.”

CLAYTON: There tends to be a natural tipping point where this siloed approach no longer delivers sufficient value to the business. The operational stress of managing too many data sources, systems and vendor relationships and the growing costs associated with that model eventually becomes unsustainable.

Regardless of which area of business is driving the change, this tipping point results in the fund looking for a data governance model and enterprise investment management platform. This enables the organisation to gain a more timely and complete view across their investments.

At this stage of their evolution, funds often need to reevaluate their operating model and clearly delineate which tools and processes can be more efficiently managed by custodians and other partners, versus those that can be internalised to deliver better overall value.

Outsourcing operations doesn’t necessarily result in a degradation of internal skillsets. Operating on the same platform as your outsourced service provider requires transparency and trust, and ensures you have a clear and auditable view of the process. Migrating portfolio management and quant tools to the platform likewise improves transparency of analytical models and code, while allowing teams to focus on generating alpha and managing risk.

FRANK: In closing, how are we helping asset owners evolve their business models to support growth?

CLAYTON: We work in lockstep with superannuation funds across their lifecycle, from custody and outsourced asset servicing to helping organisations deploy data governance and investment management solutions. Funds need the agility to respond not only to external market conditions, but also internal constraints such as resources and skills, and this is where many firms can benefit from partnering with an organisation that provides a combination of software and services. Our global scale and deep expertise across the investment process provides firms with a sustainable path to growth, whether organic or acquisition-driven.

“We work in lockstep with superannuation funds across their lifecycle, from custody and outsourced asset servicing to helping organisations deploy data governance and investment management solutions.”

PETER: Each fund has unique challenges and requirements. It is important to select a partner who utilizes industry best practices and leverages their experience to implement your vision. Our combination of asset and custody services and technology platforms provides clients with optionality at every stage of the process. Partnering with a trusted provider like State Street Alpha that understands your organisation and operational landscape can streamline and expedite the process.

Frank Smietana in conversation with Peter Sherriff and Clayton Issitt.

Our Speaking of Alpha series features insights and commentary from State Street Alpha®experts on data, operations, technology and services. Frank Smietana, our head of Thought Leadership, State Street Alpha, leads Peter Sherriff, director of Product Strategy, Asia Pacific, Charles River Development and Clayton Issitt, our head of Client Solutions, Asia Pacific, State Street Alpha, in a discussion about key operational areas impacting superannuation funds, the evolution of fund operating models and how investment and operations teams are addressing these challenges.

Director of Product Strategy, Asia Pacific Charles River

Clayton Issitt

Head of Client Solutions, Asia Pacific State Street Alpha

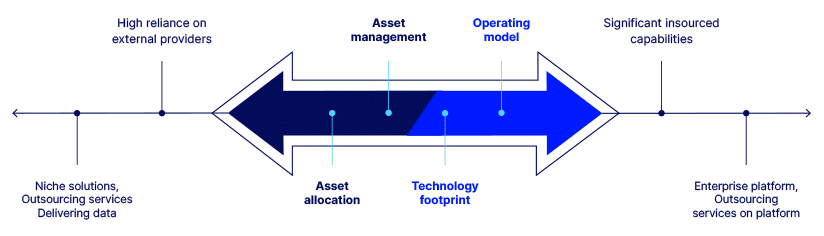

Superannuation Fund Operating Model Spectrum

“Regulatory and stakeholder demands are driving superannuation funds to evaluate their operating models, with a focus on improving efficiency, preparing for potential mergers and scaling in a sustainable fashion. Funds are navigating these challenges with different impacts.”

FRANK: Superannuation funds are generally focused on maximising value to their members. When we talk about the evolution of operating models through this lens, what are some of the key business processes and areas of technology that need to be considered?

PETER: Superannuation funds span a broad spectrum of size and sophistication across their investment and operational processes.

At the smaller end of the assets under management (AUM) scale, we see asset owners that rely heavily, or even exclusively, on their external partners and advisors to meet both investment management and reporting requirements. At the opposite end of the spectrum, there are funds that operate much like asset managers in both their global footprint and internalisation of a range of asset management and reporting capabilities.

Every organisation has various combinations of capabilities internalised, as well as an established or evolving operating model aligned with their growth plans. Inevitably, there are organisational barriers to change that need to be overcome. This can be especially challenging for funds that have largely depended on external providers, as they often lack the expertise to navigate associated complexities.

“Superannuation funds span a broad spectrum of size and sophistication across their investment and operational processes.”

FRANK: At the highest level, the asset allocation process and corresponding setting of targets and ranges is a key part of the investment decision-making process and drives member returns. In the context of the spectrum Peter just referred to, what do we see in the industry today and what are the implications for a fund seeking to increase the level of internal delegation?

CLAYTON: For many funds, targets are established at the board level, often based on advice from consultants. The fund then rebalances to these targets on a periodic basis, perhaps within a limited range of tolerance. These targets are generally reviewed and amended on a regular but relatively infrequent basis which may limit the fund’s ability to respond quickly to market conditions or take advantage of investment opportunities in a timely manner.

This can negatively impact the comparative return of funds, and by extension member outcomes, especially during market selloffs and liquidity shocks. Often, as funds increase in size and look for additional capital deployment options, a board-driven process restricts a fund’s ability to expand into new asset classes and geographies.

For the most sophisticated asset owners, responsibility for this process has been delegated to the investment team, which manages Strategy Asset Allocation (SAA) targets as well as shorter term Target Asset Allocation (TAA) goals.

Between these two extremes, we see a range of delegation, with some funds giving discretion over the setting of TAA ranges, while others limit delegation to activities like fund rebalancing, as long as it remains within the SAA range.

PETER: Interestingly, we have seen a small number of firms across Asia Pacific move away from the formal asset allocation approach and towards more of a Total Portfolio Approach (TPA). Moving to TPA represents a significant change in culture as well as process, with the team focusing on the profile of an investment opportunity and its contribution to the overall fund profile, rather than the asset class it belongs to.

Regardless of the level of delegation, we see an impact on the quantity, quality and timeliness of data needed by the investment team and the tools they use to manage investment decisions. At the simplest end of the spectrum, we see widespread dependence on spreadsheets that are fed directly by service provider data. Organisations at the sophisticated end deploy robust data management solutions and investment platforms with integrated risk and performance attribution capabilities.

The key to improved decision-making is the ‘whole of fund’ view, providing organisations with timely and accurate data on exposures and positions across internal and external managers, and public and private assets. Adopting a unified data management platform enables faster, better informed risk and allocation decisions, by reducing the traditional multi-day information lag affecting firms that are reliant on external providers and custodians for fund information.

FRANK: We have just touched on the delegation of the asset allocation process and the variations we see across the industry today. Do we typically see those top-level asset allocation decisions and the internal management of a subset of assets internalised in parallel and what does this mean from a data and technology perspective?

PETER: To some extent, the evolution of a fund’s investment capability goes hand-in-hand with the way the investment decision-making process evolves. We do see exceptions to this with some funds managing a range of investments in-house, while top level decision-making remains with the board.

The most sophisticated asset owners operate as global asset managers in their own right, with investment teams distributed across regions, managing both public and private market assets alongside multi-asset funds. These internal investment teams may be treated as simply another mandate manager by the asset allocation team or, as part of the TPA approach, they may present investment ideas and compete for capital allocation based on perceived contribution to the fund’s risk and return profile.

At the opposite end of the spectrum, where all assets are managed by external asset managers, we tend to see small investment teams that are often given a fairly broad remit to monitor external investments, provide internal board reporting and manage third-party relationships.

A broad range of investments can be managed internally. Whether it involves currency overlays, completion portfolios or individual asset class portfolios such as domestic equity, or directly managing infrastructure or real estate assets, all these have a material impact on the fund’s data and technology requirements.

“The key to improved decision-making is the “whole of fund” view, providing organisations with timely and accurate data on exposures and positions across internal and external managers and public and private assets.”

CLAYTON: We tend to see that when investment capabilities evolve, the definition of what constitutes timely, firm-wide exposure information also changes. For example, firms with limited delegation of their asset allocations and minimal internal asset management may find delayed accounting data adequate. However, firms with more delegated control over their asset allocation and significant internal asset management require an intraday view of exposures, delivered by an investment book of record (IBOR).

A longer term, SAA-only approach can be outsourced to a service provider for managing the rebalancing process, while a more active TAA/Dynamic Asset Allocation (DAA) process requires an enterprise technology solution to support internal investment and operations teams.

This incorporates a shared repository of data that addresses both manager-of-manager and internally managed assets on a common platform, as well as fit-for-purpose views for different teams based on their specific roles. Self-service analysis and reporting tools enable investment professionals to make decisions with greater confidence and collaborate more effectively.

FRANK: The timeliness, accuracy and granularity of data has been a key theme of this conversation. What are some of the considerations funds should have in mind as they evolve their technology platforms and operating models to support this increase in internalised capability?

PETER: The level of responsibility given to an investment team for making asset allocation and investment decisions is closely tied to the in-house data and technology requirements necessary to support those decisions. Where the investment team has very little control and the fund relies heavily on the board and third parties to manage investment and allocation decisions, the information provided by custodians and other service providers is generally timely enough and sufficient in terms of quantity and quality to support internal reporting needs. Typically, any management or manipulation of this data tends to be done in spreadsheets.

As funds internalise more of the investment decision-making process within their own team, there is a corresponding increase in the need for technology and data beyond that provided by the custodian. With internalisation of various aspects of the investment process being the typical evolutionary step, often in a piecemeal fashion to tightly manage costs, each internalised function or asset class is usually deployed on its own specialist or best-of-breed system. This risks creating a siloed and fragmented view of the fund’s overall investments.

We have seen a number of funds pre-emptively increase their technology footprint through data management and warehousing tools to help meet the anticipated increase in reporting and oversight obligations. This enables consolidation of custody data and enrichment with other service providers and internal data.

However, these data repositories often can’t distribute information to the deployed asset class-specific systems due to the siloed nature of these providers. As a result, funds are still heavily dependent on their custodians for an overarching view of the fund and individual investment options.

“As funds internalise more of the investment decision-making process or management within their own team, there is a corresponding increase in the need for technology and data beyond that provided by the custodian.”

CLAYTON: There tends to be a natural tipping point where this siloed approach no longer delivers sufficient value to the business. The operational stress of managing too many data sources, systems and vendor relationships and the growing costs associated with that model eventually becomes unsustainable.

Regardless of which area of business is driving the change, this tipping point results in the fund looking for a data governance model and enterprise investment management platform. This enables the organisation to gain a more timely and complete view across their investments.

At this stage of their evolution, funds often need to reevaluate their operating model and clearly delineate which tools and processes can be more efficiently managed by custodians and other partners, versus those that can be internalised to deliver better overall value.

Outsourcing operations doesn’t necessarily result in a degradation of internal skillsets. Operating on the same platform as your outsourced service provider requires transparency and trust, and ensures you have a clear and auditable view of the process. Migrating portfolio management and quant tools to the platform likewise improves transparency of analytical models and code, while allowing teams to focus on generating alpha and managing risk.

FRANK: In closing, how are we helping asset owners evolve their business models to support growth?

CLAYTON: We work in lockstep with superannuation funds across their lifecycle, from custody and outsourced asset servicing to helping organisations deploy data governance and investment management solutions. Funds need the agility to respond not only to external market conditions, but also internal constraints such as resources and skills, and this is where many firms can benefit from partnering with an organisation that provides a combination of software and services. Our global scale and deep expertise across the investment process provides firms with a sustainable path to growth, whether organic or acquisition-driven.

“We work in lockstep with superannuation funds across their lifecycle, from custody and outsourced asset servicing to helping organisations deploy data governance and investment management solutions.”

PETER: Each fund has unique challenges and requirements. It is important to select a partner who utilizes industry best practices and leverages their experience to implement your vision. Our combination of asset and custody services and technology platforms provides clients with optionality at every stage of the process. Partnering with a trusted provider like State Street Alpha that understands your organisation and operational landscape can streamline and expedite the process.

The material presented is for informational purposes only. The views expressed in this material are the views of the author, and are subject to change based on market and other conditions and factors, moreover, they do not necessarily represent the official views of Charles River Development and/or State Street Corporation and its affiliates.