Leveraging MSCI Fixed Income Models & Analytics in Charles River IMS

Jul 26, 2023

Factor-based modeling and analytics play a central role in helping portfolio managers decompose risk, facilitate stress testing, generate risk forecasts and attribute performance.

Open architecture platforms such as the Charles River Investment Management Solution (Charles River IMS) address the need for robust and flexible portfolio analytics by ensuring interoperability with a growing ecosystem of third-party providers such as MSCI, whose products, services and content are directly accessible from Charles River IMS workflows.

In this article, Steven Milanowycz and Thomas Moserdiscuss how our partnership enables faster insights for fixed income portfolio managers and analysts.

Factor-based modeling and analytics play a central role in helping portfolio managers decompose risk, facilitate stress testing, generate risk forecasts and attribute performance.

Open architecture platforms such as the Charles River Investment Management Solution (Charles River IMS) address the need for robust and flexible portfolio analytics by ensuring interoperability with a growing ecosystem of third-party providers such as MSCI, whose products, services and content are directly accessible from Charles River IMS workflows.

In this article, Steven Milanowycz and Thomas Moserdiscuss how our partnership enables faster insights for fixed income portfolio managers and analysts.

Risk factors are granular attributes of one or more asset classes that explain risk and return. Fixed income factors include interest rate, credit and prepayment risk. Factors can also include macroeconomic variables such as inflation, GDP growth, productivity, and commodity prices that impact multiple asset classes. Constructing portfolios based on established, well-researched factors, rather than asset classes, can theoretically improve portfolio diversification, minimize undesirable correlation risk, and deliver better risk-adjusted performance.

Charles River’s open architecture & interoperability with MSCI’s fixed income factor model provide firms with several benefits:

A Single, Consistent Portfolio View: Our Manager Workbench provides a single, unified desktop for managing risk and portfolio workflows, with a common data set, reference data and factor analytics. Risk exposures are updated in real time and displayed directly in the workbench, so managers can make decisions based on the latest data. Manager Workbench offers full support for factor-based risk decomposition reporting, with out-of-the-box views for active risk, risk factor contribution, tracking error and volatility.

Portfolio managers can make decisions based on the risk/return profile of individual securities and their impact on the overall portfolio and investment strategy, based on an intuitive factor model covering the full spectrum of products, sectors and global markets. MSCI’s risk analytics include differentiated capabilities in securitized products, municipal bonds and bank loans. This provides a consistent risk decomposition framework to support single security analytics. Managers can decompose relative and absolute portfolio performance with top-down and bottom-up approaches that take investment strategies into account.

Packaged Workflows: Charles River IMS provides packaged workflows that make risk and performance capabilities an integral part of the portfolio management process. These include factor model-based asset allocation, dynamic hedge construction, and portfolio stress testing. This enables asset managers to eliminate multiple point solutions and spreadsheets, so their front office teams can work more efficiently and avoid unproductive reconciliation between disparate systems.

Collaborative Decision Making: A shared, consistent view of risk metrics and asset valuations promotes collaboration across the front and middle office. Compliance officers, risk analysts, portfolio managers and traders can work more closely to implement investment ideas, manage risk, and understand the factors driving performance. A consolidated view of portfolio holdings and performance metrics also expedites client reporting activities by providing visibility into the manager’s asset allocation and targeting decisions.

Streamlined “What-if” Modeling: Interactive what-if modeling of portfolio construction and de-risking activities provides immediate feedback on how those activities will impact the portfolio. Managers can deploy MSCI’s ready-to-use, forward-looking macros, stress scenarios, and multi-period stress testing. Additionally, managers can understand portfolio risk impacts of proposed trades, compare trade ideas selectively, and incorporate compliance rules and other constraints in scenarios.

Faster Time to Information: The platform helps eliminate overnight batch processes, providing a current intraday view of the portfolio, inclusive of new securities, trade confirmations and proposed trades and their impact on the portfolio.

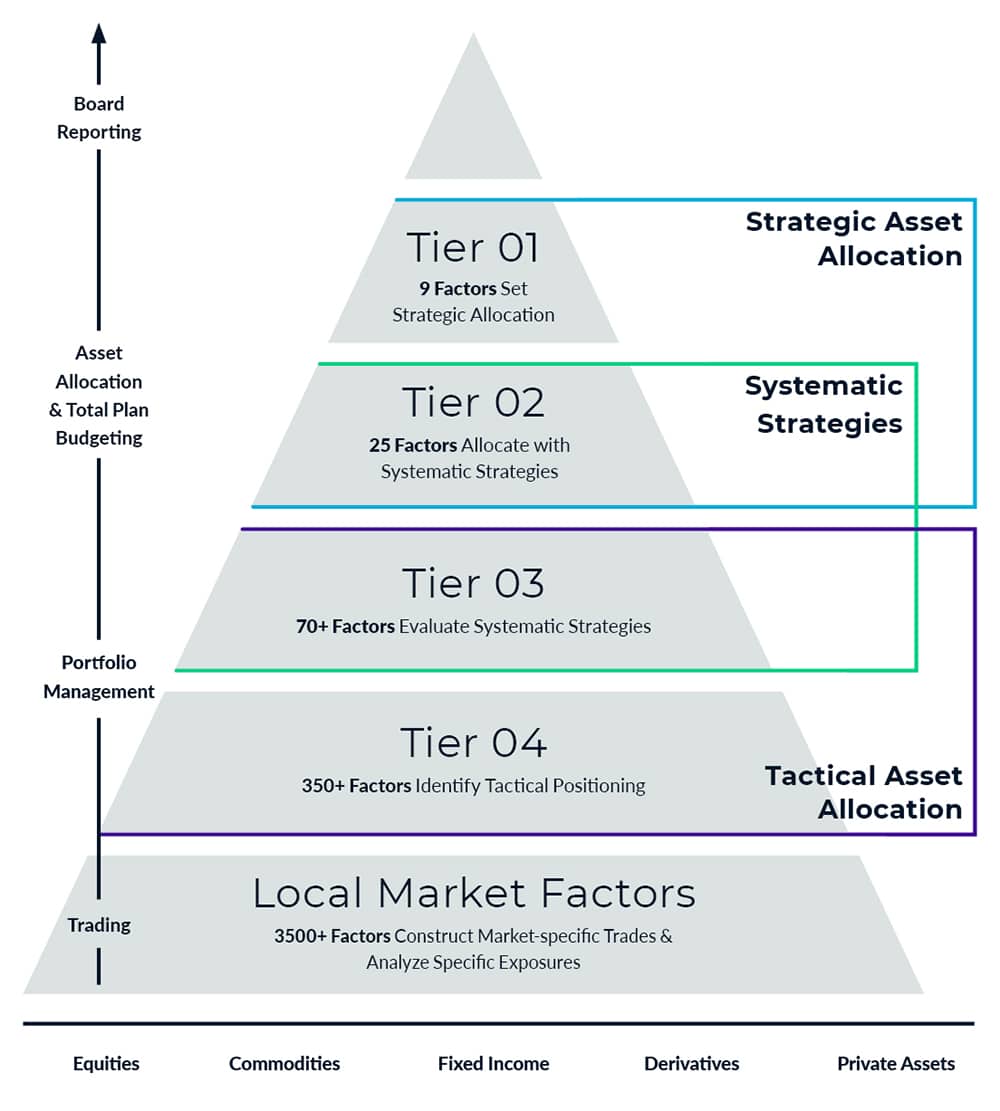

Factor hierarchy comprising the MSCI Fixed Income Factor Model

Understanding MSCI’s Fixed Income Factor Model

The Fixed Income Factor Model contains over 950+factors such as term structure factors, break-even Inflation factors, credit, swap and sovereign spread factors. The model uses option adjusted spreads (OAS) as a forward-looking indicator of risk and defines asset exposure to credit risk as ‘Duration Times Spread’ (DTS) reflecting relative changes in spread. It accounts for liquidity effects through the use of basis factors and the parsimony of credit factors is maintained to allow for easier interpretation.

*Denotes DTS Factors **As of July 2023

Understanding MSCI’s Fixed Income Factor Model

The Fixed Income Factor Model contains over 950+factors such as term structure factors, break-even Inflation factors, credit, swap and sovereign spread factors. The model uses option adjusted spreads (OAS) as a forward-looking indicator of risk and defines asset exposure to credit risk as ‘Duration Times Spread’ (DTS) reflecting relative changes in spread. It accounts for liquidity effects through the use of basis factors and the parsimony of credit factors is maintained to allow for easier interpretation.

Factor hierarchy comprising the MSCI Fixed Income Factor Model

*Denotes DTS Factors **As of July 2023

Global exposures for asset allocators

Systematic Strategy factors for manager evaluation

Detailed risk exposures for portfolio managers

The factor model consists of several integrated tiers that simplify communication of key exposures across the organization by delivering role-appropriate levels of granularity

The model covers the full spectrum of fixed income products, sectors and global markets, helping facilitate multi-asset class consistency across public and private assets. Additional features include:

A large number of credit models and dedicated factors local to the Chinese (CNY) market

Municipal bond factors developed in collaboration with leading investment managers

Bank loan factors derived from IHS Markit data

MSCI’s Fixed Income Factor Model supports required levels of granularity, from board reporting to trading:

As of July 2023

Why Charles River and MSCI?

As institutional fixed income portfolios grow in size and complexity, it’s imperative that front office investment professionals have timely and accurate analytics to understand exposures, quantify risk and helps identify potential opportunities.

“The ability to leverage MSCI factor models directly from Charles River IMS provides an enterprise-scale solution that helps facilitate collaboration between portfolio and risk managers, helps speeds time to critical information and helps enhance productivity by providing a single desktop for managing portfolio construction, scenario analysis and risk forecasting.”

About Charles River Development, A State Street Company

Investment, wealth and alternative managers, asset owners and insurers in 30 countries rely on Charles River IMS to manage USD ~$58 Trillion in assets. Together with State Street’s middle and back office services, Charles River’s cloud-deployed front office technology forms the foundation of State Street Alpha®. Charles River helps automate and simplify the investment process across asset classes, from portfolio management and risk analytics through trading and post-trade settlement, with integrated compliance and managed data throughout. Charles River’s partner ecosystem enables clients to access the data, analytics, application and liquidity providers that support their product and asset class mix. We serve clients globally with more than 1,250 employees in 11 regional offices. (Statistics as of Q2 2023)

About MSCI

MSCI is a leading provider of critical decision support tools and services for the global investment community. With over 50 years of expertise in research, data and technology, we power better investment decisions by enabling clients to understand and analyze key drivers of risk and return and confidently build more effective portfolios. We create industry-leading research-enhanced solutions that clients use to gain insight into and improve transparency across the investment process.

The material presented is for informational purposes only. The views expressed in this material are the views of the author, and are subject to change based on market and other conditions and factors, moreover, they do not necessarily represent the official views of Charles River Development and/or State Street Corporation and its affiliates.