This article addresses the limitations and risks of negative screening within separately managed accounts and the opportunities that technology and newer portfolio construction approaches offer to wealth and asset managers seeking to offer these products at scale and to retail investors who wish to personalize their portfolios according to ESG factors.

ESG investing has seen explosive growth in adoption over the last several years, accelerating through the COVID-19 crisis. In 2019, $17.1 trillion was invested in ESG-focused products, a 42% increase from 2017. In the first quarter of 2021, flows into ESG mutual funds and ETF totaled $21.5 billion, double the total from the first quarter of 2020.1 Investors want to see their values and beliefs reflected in their portfolios, and ESG is increasingly becoming a primary driver in wealth management product and service decision-making.

However, headlines concerning “greenwashing”2 by some corporations and asset managers and the breadth of distinct ESG issues have created a disconnect between the ESG objectives of individual investors and the available ESG investment products that meet those objectives. “Off-the-shelf” ESG mutual funds and ETFs may address themes of sustainability and governance, but they are too broad to capture the nuance and variety of values an individual investor may hold. Separately managed accounts (SMA) allow for the customization necessary to meet the investor’s unique ESG objectives, but the primary methodology SMAs employ to incorporate ESG today is negative screening (removing securities from the portfolio that fail to meet one or more ESG criteria). This is a blunt approach that can increase risk and doesn’t support the potential for alpha generation and other positive outcomes investors want in their ESG investments. Recent developments in optimization technology and new approaches to portfolio construction provide a better solution for the retail wealth industry: the ability to tailor individual portfolios according to ESG factors and other unique client requirements at scale.

ESG Implementation through Negative Screens

Mutual funds and ETFs are efficient vehicles for implementing investment strategies including ESG, and the market for ESG funds has grown enormously in recent years. But ESG mutual funds and ETFs generally implement broad ESG criteria designed to make those products marketable to the most investors. ESG funds utilizing broad criteria incorporate ESG factors that cover a large number of issues that may or may not be relevant or a priority for an individual investor. One investor’s ESG priorities may focus on carbon reduction and sustainable production, whereas another investor’s priority may be in ensuring good corporate governance and social justice issues in corporate management and leadership. Implementing such specific ESG objectives through pooled products is difficult or impossible.

SMAs have historically supported ESG customization through negative screening, which removes securities from the portfolio that fail to meet one or more ESG criteria. ESG data providers in the separate account industry develop and maintain lists of securities to screen for, such as companies that produce significant atmospheric carbon through coal and fossil fuel production. However, incorporating ESG restrictions into a separately managed account using negative screens creates operational and compliance complexity for the advisor, platform sponsor, and separate account manager. Individual SMA managers vary in their tolerance and willingness to accept account restrictions. More importantly, simply restricting certain securities or sectors can significantly increase the active risk within client portfolios. Offending ESG names that are restricted out of a portfolio can have unique risk/return characteristics that increase residual active risk when removed and this may negatively impact returns.

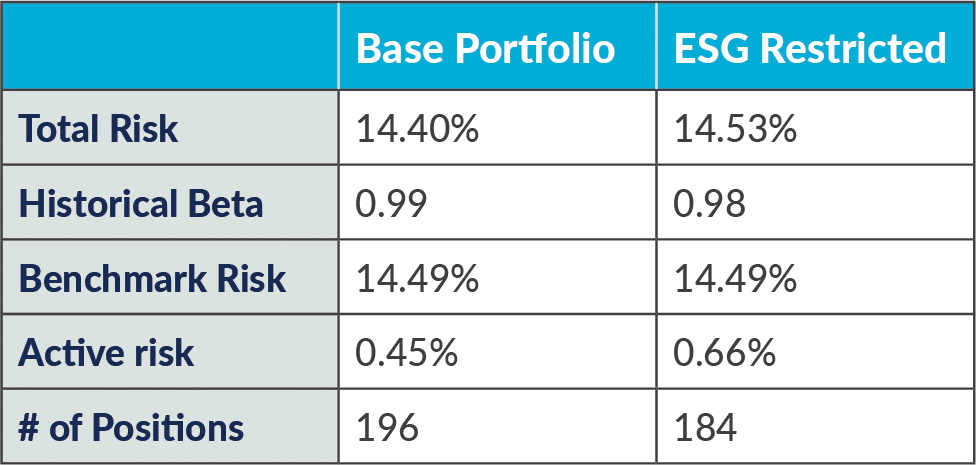

Consider a notional $250,000 client portfolio constructed two ways:

This article addresses the limitations and risks of negative screening within separately managed accounts and the opportunities that technology and newer portfolio construction approaches offer to wealth and asset managers seeking to offer these products at scale and to retail investors who wish to personalize their portfolios according to ESG factors.

ESG investing has seen explosive growth in adoption over the last several years, accelerating through the COVID-19 crisis. In 2019, $17.1 trillion was invested in ESG-focused products, a 42% increase from 2017. In the first quarter of 2021, flows into ESG mutual funds and ETF totaled $21.5 billion, double the total from the first quarter of 2020.1 Investors want to see their values and beliefs reflected in their portfolios, and ESG is increasingly becoming a primary driver in wealth management product and service decision-making.

However, headlines concerning “greenwashing”2 by some corporations and asset managers and the breadth of distinct ESG issues have created a disconnect between the ESG objectives of individual investors and the available ESG investment products that meet those objectives. “Off-the-shelf” ESG mutual funds and ETFs may address themes of sustainability and governance, but they are too broad to capture the nuance and variety of values an individual investor may hold. Separately managed accounts (SMA) allow for the customization necessary to meet the investor’s unique ESG objectives, but the primary methodology SMAs employ to incorporate ESG today is negative screening (removing securities from the portfolio that fail to meet one or more ESG criteria). This is a blunt approach that can increase risk and doesn’t support the potential for alpha generation and other positive outcomes investors want in their ESG investments. Recent developments in optimization technology and new approaches to portfolio construction provide a better solution for the retail wealth industry: the ability to tailor individual portfolios according to ESG factors and other unique client requirements at scale.

ESG Implementation through Negative Screens

Mutual funds and ETFs are efficient vehicles for implementing investment strategies including ESG, and the market for ESG funds has grown enormously in recent years. But ESG mutual funds and ETFs generally implement broad ESG criteria designed to make those products marketable to the most investors. ESG funds utilizing broad criteria incorporate ESG factors that cover a large number of issues that may or may not be relevant or a priority for an individual investor. One investor’s ESG priorities may focus on carbon reduction and sustainable production, whereas another investor’s priority may be in ensuring good corporate governance and social justice issues in corporate management and leadership. Implementing such specific ESG objectives through pooled products is difficult or impossible.

SMAs have historically supported ESG customization through negative screening, which removes securities from the portfolio that fail to meet one or more ESG criteria. ESG data providers in the separate account industry develop and maintain lists of securities to screen for, such as companies that produce significant atmospheric carbon through coal and fossil fuel production. However, incorporating ESG restrictions into a separately managed account using negative screens creates operational and compliance complexity for the advisor, platform sponsor, and separate account manager. Individual SMA managers vary in their tolerance and willingness to accept account restrictions. More importantly, simply restricting certain securities or sectors can significantly increase the active risk within client portfolios. Offending ESG names that are restricted out of a portfolio can have unique risk/return characteristics that increase residual active risk when removed and this may negatively impact returns.

Consider a notional $250,000 client portfolio constructed two ways:

A Base Portfolio (with no ESG restrictions) is constructed solely to minimize forecasted tracking error or Active Risk to an equity benchmark.

An ESG Restricted Portfolio eliminates 12 individual securities from the portfolio that violate a typical ESG screen around carbon generation.

This simple example demonstrates how restricting securities from a portfolio using negative screens increases active risk.

In this example, the active risk in the notional client portfolio increased from 0.45% to 0.66% by removing the 12 offending securities. This increase in risk represents the increased likelihood that the customer’s return will be different from the return of the underlying benchmark, which in this case is the S&P 500.

Increased risk is not the only downside to utilizing negative screens in ESG portfolio construction, even when using an optimization-based investment process. Negative screens ultimately limit the potential positive outcomes for the investor. Restrictions are binary (leave the stock in or take it out), and removal of offending names doesn’t allow for any nuanced implementation that weighs the relative positive or negative merits of individual securities by any ESG criteria. Restrictions are suitable for simplistically eliminating offending securities, but provides no upside potential or means for positively tilting the portfolio towards ESG-positive names or factors.

Modern Approaches in ESG Implementation

The increased demand for ESG-customized investment products and the limitations of negative screens have set the stage for innovation in technology tools and applications and ESG portfolio construction processes.

Reducing Risk through Portfolio Optimization

A portfolio optimizer can be used to mitigate potential increased risk associated with negative screening. Optimizers and risk models are used primarily in institutional portfolio management to construct sophisticated portfolios to meet very specific risk/return/exposure characteristics required for institutions and funds. Optimizers are complex, computationally intensive and potentially time-consuming to use, and sometimes create edge-case trade and portfolio recommendations that can be difficult to understand for individual investors and advisors. But advances in technology and operational delivery capabilities within wealth management platforms now support efficient use of optimizers and risk models, enabling better ESG solutions for investors. Optimization-based systems are able to construct a portfolio unique to the individual investor including ESG objectives, while simultaneously managing risk and individual investor tax impact. A portfolio optimizer can reduce the active risk from negative screening, and also tilt the portfolio based on client ESG preferences and associated factors.

The system achieves this by re-weighting the portfolio to minimize the risk impact of removing the offending securities. Therefore, when securities are excluded based on an ESG negative screen (e.g. exclude three high-carbon securities that represent 4% of the portfolio), the optimizer can overweight or underweight the other securities to offset the missing factor risks/exposures associated with the restricted securities.

Example 1 (Click to Enlarge)

This simple example demonstrates how restricting securities from a portfolio using negative screens increases active risk.

Example 1 (Click to Enlarge)

In this example, the active risk in the notional client portfolio increased from 0.45% to 0.66% by removing the 12 offending securities. This increase in risk represents the increased likelihood that the customer’s return will be different from the return of the underlying benchmark, which in this case is the S&P 500.

Increased risk is not the only downside to utilizing negative screens in ESG portfolio construction, even when using an optimization-based investment process. Negative screens ultimately limit the potential positive outcomes for the investor. Restrictions are binary (leave the stock in or take it out), and removal of offending names doesn’t allow for any nuanced implementation that weighs the relative positive or negative merits of individual securities by any ESG criteria. Restrictions are suitable for simplistically eliminating offending securities, but provides no upside potential or means for positively tilting the portfolio towards ESG-positive names or factors.

Modern Approaches in ESG Implementation

The increased demand for ESG-customized investment products and the limitations of negative screens have set the stage for innovation in technology tools and applications and ESG portfolio construction processes.

Reducing Risk through Portfolio Optimization

A portfolio optimizer can be used to mitigate potential increased risk associated with negative screening. Optimizers and risk models are used primarily in institutional portfolio management to construct sophisticated portfolios to meet very specific risk/return/exposure characteristics required for institutions and funds. Optimizers are complex, computationally intensive and potentially time-consuming to use, and sometimes create edge-case trade and portfolio recommendations that can be difficult to understand for individual investors and advisors. But advances in technology and operational delivery capabilities within wealth management platforms now support efficient use of optimizers and risk models, enabling better ESG solutions for investors. Optimization-based systems are able to construct a portfolio unique to the individual investor including ESG objectives, while simultaneously managing risk and individual investor tax impact. A portfolio optimizer can reduce the active risk from negative screening, and also tilt the portfolio based on client ESG preferences and associated factors.

The system achieves this by re-weighting the portfolio to minimize the risk impact of removing the offending securities. Therefore, when securities are excluded based on an ESG negative screen (e.g. exclude three high-carbon securities that represent 4% of the portfolio), the optimizer can overweight or underweight the other securities to offset the missing factor risks/exposures associated with the restricted securities.

In the previous example, we constructed an ESG Restricted portfolio that excluded a number of names representative of a low-carbon ESG filter.

If we use the optimizer to recreate the portfolio from the original investable universe (in this case, the S&P 500) but in light of those same carbon restrictions, the system can create a portfolio with virtually the same active risk (0.46% as compared to 0.45%) as the original non-restricted portfolio. Even in the application of simplistic negative screens, an optimization-based investment process can substantially reduce or eliminate the active risk that can be introduced by screening out securities.

ESG-Based Portfolio Optimization

Newer ESG-based portfolio construction approaches focus on adding alpha and/or managing unique risk by incorporating ESG factors directly into the optimization process. Optimization of a portfolio around an ESG factor can allow much more nuanced and granular tilts based on both positive and negative ESG considerations.

When combined with traditional measures of portfolio risk against broad market benchmarks and the calculation of individual tax impact to the investor, this type of investment process is more likely to deliver on the individual investor’s requirements in all areas – ESG compliance, risk, and tax.

Integrating Process, Technology, and Data for ESG Customization

This level of ESG portfolio customization requires considerable data about the investor – their ESG values and preferences, risk tolerance, and individual tax objectives and tax rates in order to support a tax-efficient implementation. Some of this data is relatively static and can be captured during account opening, but much of it changes dynamically (e.g. the ESG characteristics of individual securities or the client’s tax budget.) A custom ESG portfolio also requires a custom ESG report for sharing with the investor their ESG value/compliance against their objectives.

To capture and integrate the necessary data efficiently, customized ESG portfolios require an integrated process with three primary components:

Example 2 (Click to Enlarge)

Example 2 (Click to Enlarge)

In the previous example, we constructed an ESG Restricted portfolio that excluded a number of names representative of a low-carbon ESG filter.

If we use the optimizer to recreate the portfolio from the original investable universe (in this case, the S&P 500) but in light of those same carbon restrictions, the system can create a portfolio with virtually the same active risk (0.46% as compared to 0.45%) as the original non-restricted portfolio. Even in the application of simplistic negative screens, an optimization-based investment process can substantially reduce or eliminate the active risk that can be introduced by screening out securities.

ESG-Based Portfolio Optimization

Newer ESG-based portfolio construction approaches focus on adding alpha and/or managing unique risk by incorporating ESG factors directly into the optimization process. Optimization of a portfolio around an ESG factor can allow much more nuanced and granular tilts based on both positive and negative ESG considerations.

When combined with traditional measures of portfolio risk against broad market benchmarks and the calculation of individual tax impact to the investor, this type of investment process is more likely to deliver on the individual investor’s requirements in all areas – ESG compliance, risk, and tax.

Integrating Process, Technology, and Data for ESG Customization

This level of ESG portfolio customization requires considerable data about the investor – their ESG values and preferences, risk tolerance, and individual tax objectives and tax rates in order to support a tax-efficient implementation. Some of this data is relatively static and can be captured during account opening, but much of it changes dynamically (e.g. the ESG characteristics of individual securities or the client’s tax budget.) A custom ESG portfolio also requires a custom ESG report for sharing with the investor their ESG value/compliance against their objectives.

To capture and integrate the necessary data efficiently, customized ESG portfolios require an integrated process with three primary components:

ESG Client Discovery & Solution Development – the digital experience to capture client ESG preferences and other traditional risk profiling & suitability assessments resulting in a target portfolio and Investment Policy Statement (IPS).

Portfolio Implementation – the system for constructing an optimal portfolio based on the client’s specific requirements and cost/risk constraints (e.g. minimum trade size, forecasted tracking error allowances), implementation and execution in the market, along with all associated account operations based on changes in client need, input data, and market movement on an ongoing basis.

Impact Analysis & Reporting – the ongoing process of measuring and reporting back ESG compliance, impact, and other traditional performance and risk measurements.

ESG Client Discovery & Solution Development

The process to identify and implement a client’s ESG preferences is data-driven and requires analysis for ESG impact as well as risk/performance. Innovative ESG digital experience’s have been developed to facilitate the discovery process of a customer’s ESG values, helping the investor and advisor understand and assess the trade-offs of ESG factor tilts. These digital experiences provide detailed analytics and portfolio comparison tools that highlight specific ESG value and/or impact assessments.

ESG data providers have a critical role in supporting ESG client discovery and implementation. Their data sets allow greater visibility into corporate ESG practices and performance against a wide array of ESG issues and associated measures. Granular ESG factor and performance data enables impact visualization and analytics that give advisors and investors a clear understanding of the expected value and impact to their portfolio construction decisions, including potential risks.

The output of the client ESG values and needs discovery becomes the set of inputs that will govern ESG decision-making within the ongoing portfolio management process, and is typically codified in the customer’s investment policy statement. In some cases, the initial ESG discovery process results in a static target portfolio, allowing the advisor and customer to know exactly which securities the portfolio will hold. This works particularly well in client self-directed journeys or advisor-discretionary programs in which the individual investor may need or want to know the exact portfolio composition as part of the investment decision and sale. In other instances, the ESG inputs are applied in real time based on changing ESG and risk data values, resulting in a more dynamically-managed portfolio. This is the structure utilized by third-party specialist ESG SMA managers or managed account platforms that create a dynamic model based on changing data and client inputs.become the preferred “best practice” for individual investors within the wealth management industry.

ESG Portfolio Implementation

ESG portfolio optimization can be done by any portfolio manager – a financial advisor operating in a discretionary rep-as-portfolio manager structure, a central home-office portfolio management team, or a third-party operating within a separate account program. Optimization-based investment processes produce trade recommendations and other data that allow the portfolio manager to understand the trade recommendations and ensure compliance with the client’s investment objectives. The rationale for an optimization-based trade recommendation may be less clear than in a traditional rules-based rebalancing process. For this reason, the portfolio manager must review specific metrics, such as projected tracking error or compliance with a customer’s tax budget to ensure client portfolios are within operating tolerances.

While not explicitly related to ESG personalization, the optimization-based investment process used to manage ESG personalization can also tailor portfolios for individual tax circumstances, known as tax optimization. Tax optimization involves making client-specific decisions to improve the after-tax return of the ESG portfolio strategy by seeking to reduce taxable gains, maintain realized gains at long-term capital gains rates, and harvest losses to use against external or future taxable gains. Research from leading providers of tax optimization cite that 40 basis points up to 200 basis points of incremental after-tax return can be generated through tax optimization of investor portfolios. In addition to capturing ESG values and preferences, the digital experience for an ESG customization program should also capture and maintain customer-specific settings used for tax optimization, such as individual tax rates and tax budget. Personalized ESG platforms must support tax optimization as a means of improving after-tax return in order to deliver the maximum value for wealth customers.

ESG Impact Analysis, Reporting, & Compliance

In addition to allowing investors to express their views on ESG topics, ESG investing creates the added layer of understanding how those investment decisions have led to measurable change. For example, investors concerned with making investments to reduce their carbon footprint need a reporting framework demonstrating how their portfolio holdings have done that. Since core sustainability themes take time to execute, there is a need for a robust time series of relevant metrics so investors can monitor these KPIs over time and track any trends to adjust the portfolio as required. As investors implement ESG strategies, the need for integrating ESG data into compliance processes also becomes critical. Asset and wealth management organizations will have increasing need to monitor and reporting compliance against both client ESG objectives as well as firm-level ESG measurements and objectives.

Conclusion

While ESG investing principles aren’t new, the technology, data, and business practice around implementing ESG customization based on the ESG values and preferences of individual wealth investors is evolving quickly. The old way of simplistic negative screening is insufficient and can create unacceptable levels of active risk. Modern ESG portfolio management practices can now be implemented for individual investors at scale, utilizing ESG risk data and portfolio optimization technology. As more tailored ESG investing platforms launch in the coming years, personalized ESG implementation will become the preferred “best practice” for individual investors within the wealth management industry.

ESG Factors for Optimization

To simplify implementation, many ESG data providers have created aggregated data sets that synthesize and normalize multiple ESG inputs to derive factors designed specifically for broad market ESG portfolio optimization. The use of these multi-disciplined ESG factors allows for efficient construction of ESG portfolios spanning the efficient frontier, designed to meet the specific risk tolerance and ESG priorities of individual investors.

As one example, State Street Global Advisors has created their R-Factor™ ESG score. R-Factor™ scores draw on multiple data sources and leverage widely accepted, transparent materiality frameworks from the Sustainability Accounting Standards Board (SASB) and corporate governance codes to generate a unique ESG score for listed companies.

Carbon Factors

ESG personalization can also be more targeted using narrower ESG factors such as negatively screening out carbon-producing companies such as coal producers, and then optimizing around a carbon impact factor that could over-weight securities that are specifically addressing carbon reduction. Alternatively, the portfolio could be optimized for a single factor such as carbon intensity while staying within a projected tracking error threshold of the broad equity market index, resulting in a portfolio tailored narrowly to reduce the carbon impact of holdings.

The benefits of using narrower ESG factors such as carbon reduction is an improved ability to assess and communicate actual impact on the ESG issues that might matter most to the investor. While it’s technically feasible to optimize across multiple underlying ESG factors simultaneously, complexity increases exponentially with the addition of ESG factors to the investment process, and the ‘understandability’ of the resultant portfolio goes down. This makes the multi-dimensional ESG factors good optimization inputs for wealth ESG personalization.

ESG Client Discovery & Solution Development

The process to identify and implement a client’s ESG preferences is data-driven and requires analysis for ESG impact as well as risk/performance. Innovative ESG digital experience’s have been developed to facilitate the discovery process of a customer’s ESG values, helping the investor and advisor understand and assess the trade-offs of ESG factor tilts. These digital experiences provide detailed analytics and portfolio comparison tools that highlight specific ESG value and/or impact assessments.

ESG data providers have a critical role in supporting ESG client discovery and implementation. Their data sets allow greater visibility into corporate ESG practices and performance against a wide array of ESG issues and associated measures. Granular ESG factor and performance data enables impact visualization and analytics that give advisors and investors a clear understanding of the expected value and impact to their portfolio construction decisions, including potential risks.

The output of the client ESG values and needs discovery becomes the set of inputs that will govern ESG decision-making within the ongoing portfolio management process, and is typically codified in the customer’s investment policy statement. In some cases, the initial ESG discovery process results in a static target portfolio, allowing the advisor and customer to know exactly which securities the portfolio will hold. This works particularly well in client self-directed journeys or advisor-discretionary programs in which the individual investor may need or want to know the exact portfolio composition as part of the investment decision and sale. In other instances, the ESG inputs are applied in real time based on changing ESG and risk data values, resulting in a more dynamically-managed portfolio. This is the structure utilized by third-party specialist ESG SMA managers or managed account platforms that create a dynamic model based on changing data and client inputs.become the preferred “best practice” for individual investors within the wealth management industry.

ESG Portfolio Implementation

ESG portfolio optimization can be done by any portfolio manager – a financial advisor operating in a discretionary rep-as-portfolio manager structure, a central home-office portfolio management team, or a third-party operating within a separate account program. Optimization-based investment processes produce trade recommendations and other data that allow the portfolio manager to understand the trade recommendations and ensure compliance with the client’s investment objectives. The rationale for an optimization-based trade recommendation may be less clear than in a traditional rules-based rebalancing process. For this reason, the portfolio manager must review specific metrics, such as projected tracking error or compliance with a customer’s tax budget to ensure client portfolios are within operating tolerances.

While not explicitly related to ESG personalization, the optimization-based investment process used to manage ESG personalization can also tailor portfolios for individual tax circumstances, known as tax optimization. Tax optimization involves making client-specific decisions to improve the after-tax return of the ESG portfolio strategy by seeking to reduce taxable gains, maintain realized gains at long-term capital gains rates, and harvest losses to use against external or future taxable gains. Research from leading providers of tax optimization cite that 40 basis points up to 200 basis points of incremental after-tax return can be generated through tax optimization of investor portfolios. In addition to capturing ESG values and preferences, the digital experience for an ESG customization program should also capture and maintain customer-specific settings used for tax optimization, such as individual tax rates and tax budget. Personalized ESG platforms must support tax optimization as a means of improving after-tax return in order to deliver the maximum value for wealth customers.

ESG Impact Analysis, Reporting, & Compliance

In addition to allowing investors to express their views on ESG topics, ESG investing creates the added layer of understanding how those investment decisions have led to measurable change. For example, investors concerned with making investments to reduce their carbon footprint need a reporting framework demonstrating how their portfolio holdings have done that. Since core sustainability themes take time to execute, there is a need for a robust time series of relevant metrics so investors can monitor these KPIs over time and track any trends to adjust the portfolio as required. As investors implement ESG strategies, the need for integrating ESG data into compliance processes also becomes critical. Asset and wealth management organizations will have increasing need to monitor and reporting compliance against both client ESG objectives as well as firm-level ESG measurements and objectives.

Conclusion

While ESG investing principles aren’t new, the technology, data, and business practice around implementing ESG customization based on the ESG values and preferences of individual wealth investors is evolving quickly. The old way of simplistic negative screening is insufficient and can create unacceptable levels of active risk. Modern ESG portfolio management practices can now be implemented for individual investors at scale, utilizing ESG risk data and portfolio optimization technology. As more tailored ESG investing platforms launch in the coming years, personalized ESG implementation will become the preferred “best practice” for individual investors within the wealth management industry.

ESG Factors for Optimization

To simplify implementation, many ESG data providers have created aggregated data sets that synthesize and normalize multiple ESG inputs to derive factors designed specifically for broad market ESG portfolio optimization. The use of these multi-disciplined ESG factors allows for efficient construction of ESG portfolios spanning the efficient frontier, designed to meet the specific risk tolerance and ESG priorities of individual investors.

As one example, State Street Global Advisors has created their R-Factor™ ESG score. R-Factor™ scores draw on multiple data sources and leverage widely accepted, transparent materiality frameworks from the Sustainability Accounting Standards Board (SASB) and corporate governance codes to generate a unique ESG score for listed companies.

Carbon Factors

ESG personalization can also be more targeted using narrower ESG factors such as negatively screening out carbon-producing companies such as coal producers, and then optimizing around a carbon impact factor that could over-weight securities that are specifically addressing carbon reduction. Alternatively, the portfolio could be optimized for a single factor such as carbon intensity while staying within a projected tracking error threshold of the broad equity market index, resulting in a portfolio tailored narrowly to reduce the carbon impact of holdings.

The benefits of using narrower ESG factors such as carbon reduction is an improved ability to assess and communicate actual impact on the ESG issues that might matter most to the investor. While it’s technically feasible to optimize across multiple underlying ESG factors simultaneously, complexity increases exponentially with the addition of ESG factors to the investment process, and the ‘understandability’ of the resultant portfolio goes down. This makes the multi-dimensional ESG factors good optimization inputs for wealth ESG personalization.

All Insights

This article originally appeared in the Third Quarter 2021 edition of the MMI Journal of Investment Advisory Solutions.

1 Source: Munk, Cheryl Winokur, June 27, 2021, “The New Math of Socially Responsible Investing,” The Wall Street Journal, www.wsj.com/articles/socially-responsible-investing-11624288038

2 Sources: Adamczyck, Alicia, April 23, 2021, “Why ‘greenwashing’ is an issue for sustainable investments – and how to avoid it,” cnbc.com, www.cnbc.com/2021/04/23/what-to-know-about-greenwashing-in-sustainable-investments.html

Mooney, Attracta, March 10, 2021, “Greenwashing in finance: Europe’s push to police ESG Investing,” Financial Times, www.ft.com/content/74888921-368d-42e1-91cd-c3c8ce64a05e

Contact Us

To learn more about our Wealth Management Solution or to schedule a demo.

3721001.1.1.GBL.

The material presented is for informational purposes only. The views expressed in this material are the views of the author, and are subject to change based on market and other conditions and factors, moreover, they do not necessarily represent the official views of Charles River Development and/or State Street Corporation and its affiliates.